Table of Contents

- Types of Home Loans

- Factors to Consider When Choosing a Home Loan

- 5 Top Home Loan Providers in India

- State Bank of India Updated Interest Rates 2024

- HDFC Bank Home loans Updated Interest Rates 2024

- ICICI Bank Home Loans Updated Interest Rate 2024

- Axis Bank Home Loans Updated Interest Rates 2024

- Bank of Baroda Home Loans Updated Interest Rates 2024

- Advantages of Taking A Home Loan

- Conclusion

- Faq's

Home loans are a popular choice for Indians looking to purchase their dream home. With rising property prices, most homebuyers rely on home loans to finance their purchase. However, with numerous lenders offering a wide range of home loan options, it can be challenging to determine the best home loan for your needs.

In this article, we will explore some of the best home loans available in India and the factors to consider when choosing a home loan.

Types of Home Loans

Types of Home Loans

Types of Home Loans

Fixed-rate home loans: These loans offer a fixed interest rate throughout the loan tenure, providing stability and predictability in monthly payments.

Floating-rate home loans: These loans have an interest rate that fluctuates based on market conditions and the lender's benchmark rate. While the interest rate may change, these loans often offer lower initial rates compared to fixed-rate loans.

Affordable housing loans: These loans are designed for low-income borrowers looking to purchase affordable housing units. They typically have lower interest rates and longer repayment tenures.

Also Read: A Guide On Non-Scheduled Banks In India

Factors to Consider When Choosing a Home Loan

Interest rates: Compare interest rates offered by different lenders to find the most competitive rate. Keep in mind that the actual interest rate may vary based on your creditworthiness and other factors.

Loan tenure: Choose a loan tenure that aligns with your financial goals and repayment capacity. A longer tenure will result in lower monthly payments but higher overall interest costs.

Loan amount: Ensure that the loan amount is sufficient to cover the cost of your desired property, including any additional fees or charges.

Tax benefits: Home loan borrowers can claim tax deductions on the interest paid and the principal repaid, subject to certain limits.

Lender's reputation: Choose a reputable lender with a strong track record and good customer service.

Tenure Flexibility: Opting for a home loan with a suitable repayment tenure ensures that the Equated Monthly Installments (EMIs) are manageable and align with your financial capabilities without straining your lifestyle.

Hidden Fees & Charges: Being aware of potential hidden fees like loan processing fees and bounce charges helps in understanding the total cost of the loan and avoiding any financial surprises during the repayment period.

Repayment Capability: Evaluating your repayment capability based on current and future income, considering factors like retirement, alternative income sources, and unexpected expenses, helps in determining the loan amount you can comfortably afford.

Taxation: Understanding the tax benefits associated with a home loan, such as tax rebates under Section 24 and Section 80C, can help in maximizing savings and reducing the overall cost of borrowing.

5 Top Home Loan Providers in India

S.No Bank Name Interest Rate Processing Fees 1 SBI Home Loan Starting from 8.50% 0.35% of the loan amount plus applicable GST, minimum Rs.2,000/- plus applicable GST and maximum of Rs. 10,000/- plus applicable GST 2 HDFC Home Loan Starting from 8.75% Up to 0.50% of the loan amount or INR 3,000, whichever is higher, plus applicable taxes. 3 Axis Bank Home Loan Starting from 8.75% Up to 1% of the loan amount subject to a minimum of INR 10,000. Upfront processing fee of INR 2,500 + GST. 4 ICICI Home Loan Starting from 9:25% Up to 1.00% of the loan amount + GST. 5 Bank of Baroda Home Loan Starting From 8.40% Up to 0.50% of the loan amount or a maximum of INR 7,500 + GST.

| S.No | Bank Name | Interest Rate | Processing Fees |

|---|---|---|---|

| 1 | SBI Home Loan | Starting from 8.50% | 0.35% of the loan amount plus applicable GST, minimum Rs.2,000/- plus applicable GST and maximum of Rs. 10,000/- plus applicable GST |

| 2 | HDFC Home Loan | Starting from 8.75% | Up to 0.50% of the loan amount or INR 3,000, whichever is higher, plus applicable taxes. |

| 3 | Axis Bank Home Loan | Starting from 8.75% | Up to 1% of the loan amount subject to a minimum of INR 10,000. Upfront processing fee of INR 2,500 + GST. |

| 4 | ICICI Home Loan | Starting from 9:25% | Up to 1.00% of the loan amount + GST. |

| 5 | Bank of Baroda Home Loan | Starting From 8.40% | Up to 0.50% of the loan amount or a maximum of INR 7,500 + GST. |

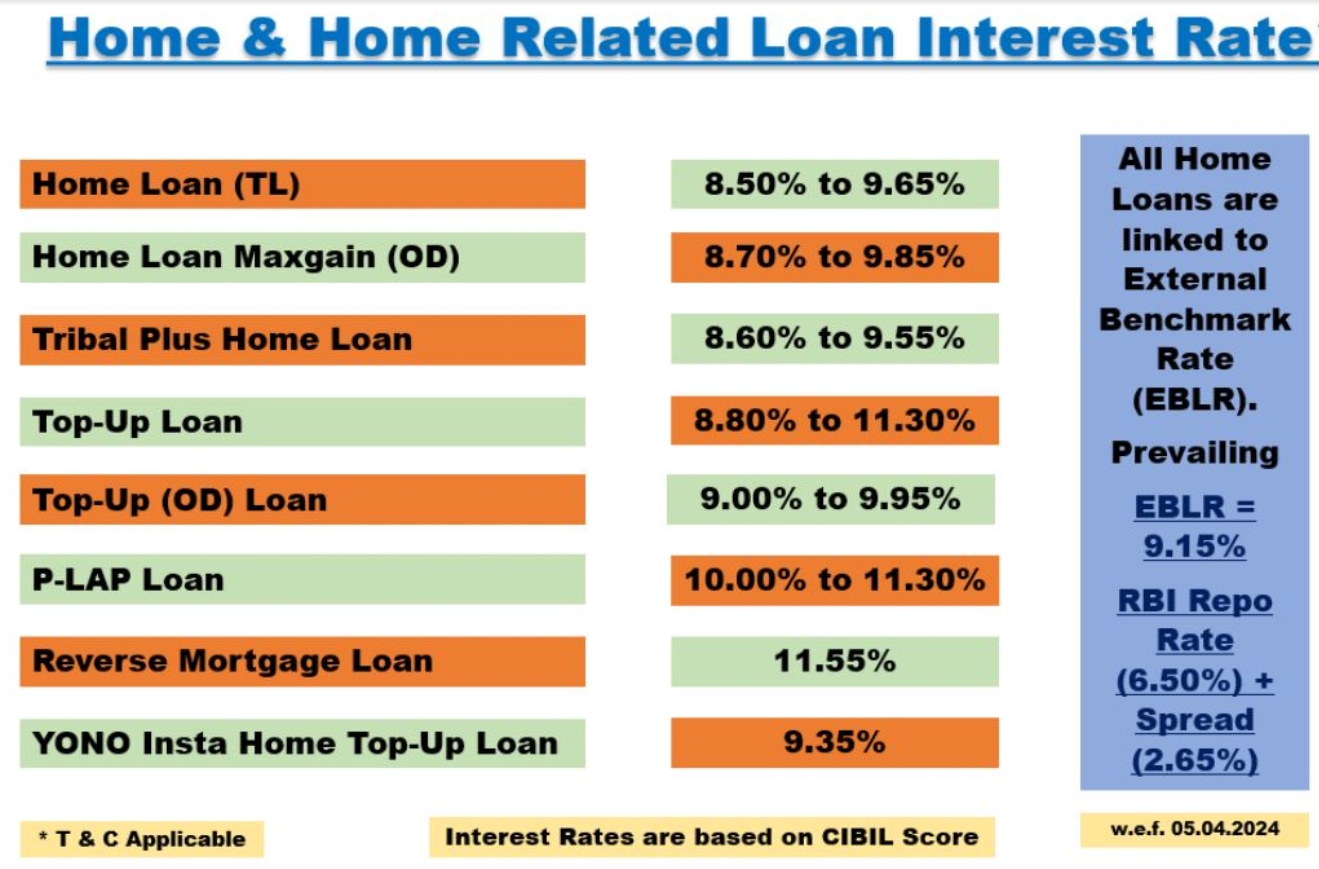

State Bank of India Updated Interest Rates 2024

SBI is the largest lender in India and offers home loans at a competitive interest rate starting from 8.50% per annum.

Updated Home Loan Interest Rates of SBI Bank

Image Source: SBI Official website

Features of SBI Home Loan

Low Processing Fee

No Hidden Charges

No Pre Payment Penalty

Interest charges on Daily Reducing Balance

Repayment up to 30 years

Home Loan Available as Overdraft

Interest Concession for Women Borrowers

Eligibility for SBI Home Loan

Resident Type: Resident Indian

Minimum Age: 18 years

Maximum Age: 70 years

Loan Tenure: up to 30 years

Documents Required For SBI Home Loan

Employer Identity Card

Loan Application: Completed loan application form duly filled in affixed with 3 Passport size photographs

Proof of Identity (Any one): PAN/ Passport/ Driver's License/ Voter ID card

Proof of Residence/ Address (Any one): Recent copy of Telephone Bill/ Electricity Bill/Water Bill/ Piped Gas Bill or copy of Passport/ Driving License/ Aadhar Card

Property Papers:

Permission for construction (where applicable)

Registered Agreement for Sale (only for Maharashtra)/Allotment Letter/Stamped Agreement for Sale

Occupancy Certificate (in case of ready to move property)

Share Certificate (only for Maharashtra), Maintenance Bill, Electricity Bill, Property Tax Receipt

Approved Plan copy (Xerox Blueprint) & Registered Development Agreement of the builder, Conveyance Deed (For New Property)

Payment Receipts or bank A/C statement showing all the payments made to Builder/Seller

Account Statement:

Last 6 months Bank Account Statements for all Bank Accounts held by the applicant/s

If any previous loan from other Banks/Lenders, then Loan A/C statement for last 1 year

Income Proof for Salaried Applicant/ Co-applicant/ Guarantor:

Salary Slip or Salary Certificate of last 3 months

Copy of Form 16 for last 2 years or copy of IT Returns for last 2 financial years, acknowledged by IT Dept.

Income Proof for Non-Salaried Applicant/ Co-applicant/ Guarantor:

Business address proof

IT returns for last 3 years

Balance Sheet & Profit & Loss A/c for last 3 years

Business License Details(or equivalent)

TDS Certificate (Form 16A, if applicable)

Certificate of qualification (for C.A./ Doctor and other professionals)

HDFC Bank Home loans Updated Interest Rates 2024

HDFC Bank Home Loan offers an attractive range of interest rates from 8.75% to 9.65%catering to a wide spectrum of home buyers. Known for its customer-friendly approach, HDFC Bank provides flexible loan options with competitive processing fees. The bank's extensive network, robust customer service, and innovative digital solutions enhance the home loan experience, ensuring borrowers receive personalised support and efficient service throughout the loan process.

Official site: https://www.hdfc.com/housing-loans/home-loans

Documents Required For HDFC Home Loan

For identity and residence proof

PAN card

Passport

Aadhar card

Driving license

Government-issued identification

Account Statement For Salaried

Last 3 months' salary slips

6 months bank statements reflecting salary credits

Latest Form-16 and IT returns

For the self-employed

Income tax returns

Balance sheets

Profit and loss statements for the last 2 years

Business entity statements attested by a CA

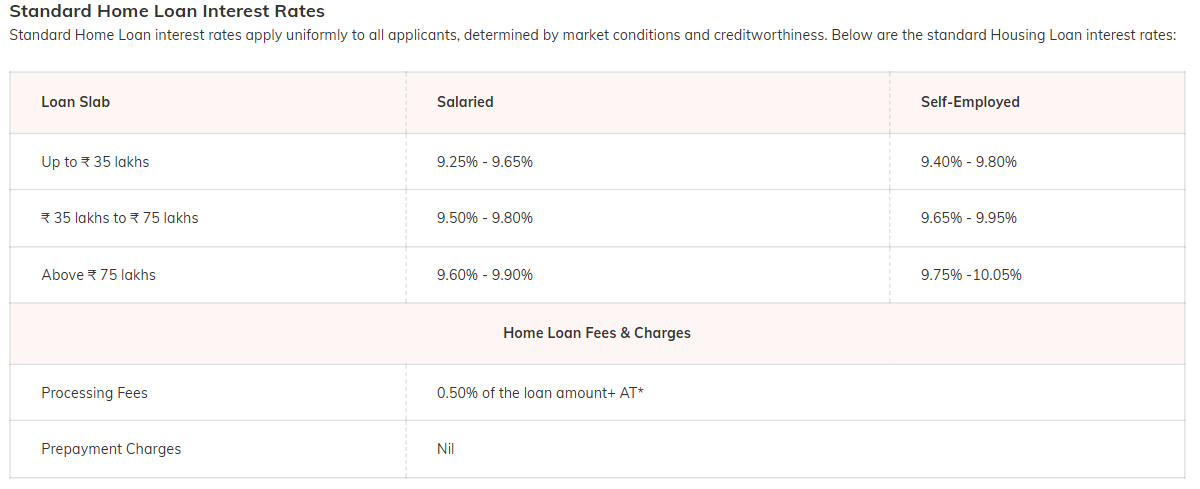

ICICI Bank Home Loans Updated Interest Rate 2024

ICICI Bank offers housing loans to eligible borrowers at competitive interest rates starting at 9.25% per annum, with loan terms extending up to 30 years and flexible repayment options.Additionally, ICICI Bank partners with the Pradhan Mantri Awas Yojana (PMAY) scheme, providing an added advantage for homebuyers. This makes ICICI Bank a top choice for housing loans, combining affordability with extensive support for customers

Official site: https://www.icicibank.com/personal-banking/loans/home-loan

Eligibility

To secure a Home Loan and make your dream of owning a home a reality, it is essential to meet certain eligibility criteria. Lenders in India consider several factors when determining your eligibility for a Home Loan.

Here's a detailed overview of the loan eligibility criteria:

20 to 65 years for salaried individuals

21 to 70 years for self-employed individuals

Income

Minimum salary of Rs 25,000, Employment Stability

Self-employed: Stable business track record

Credit Score

A good credit score of 700 and above

Nationality

Indian

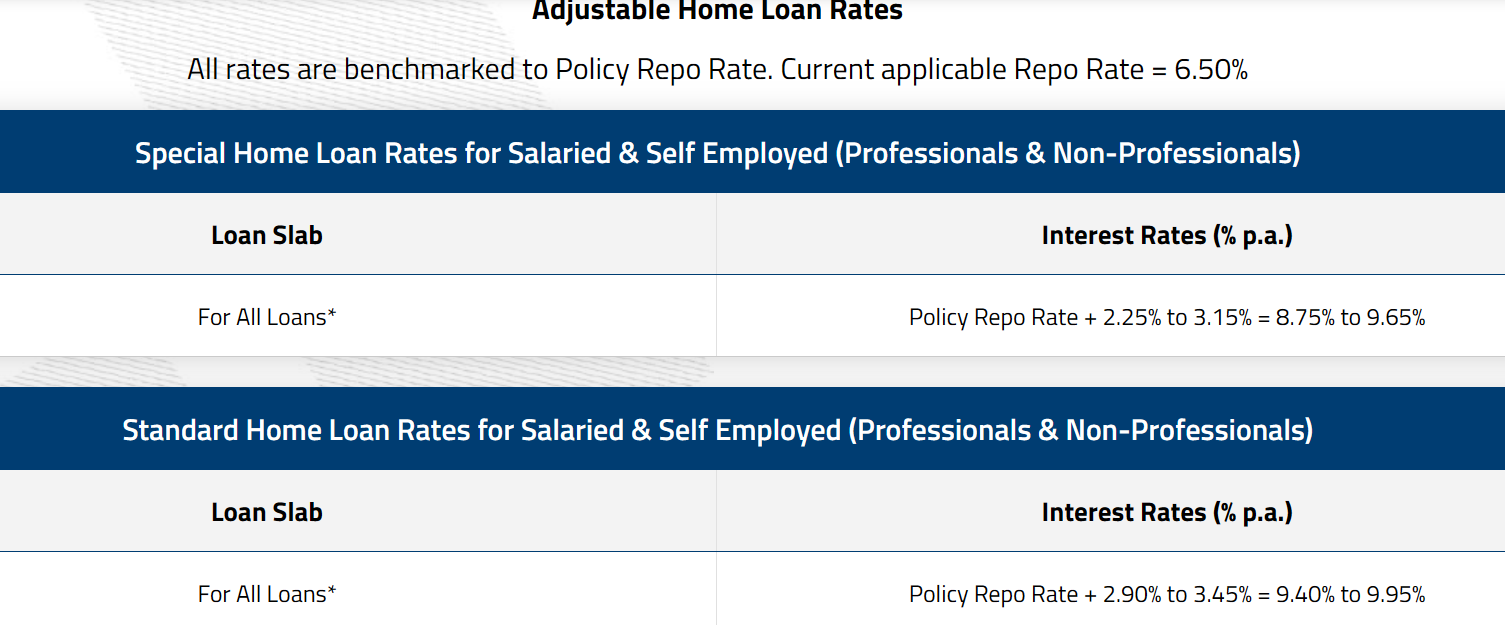

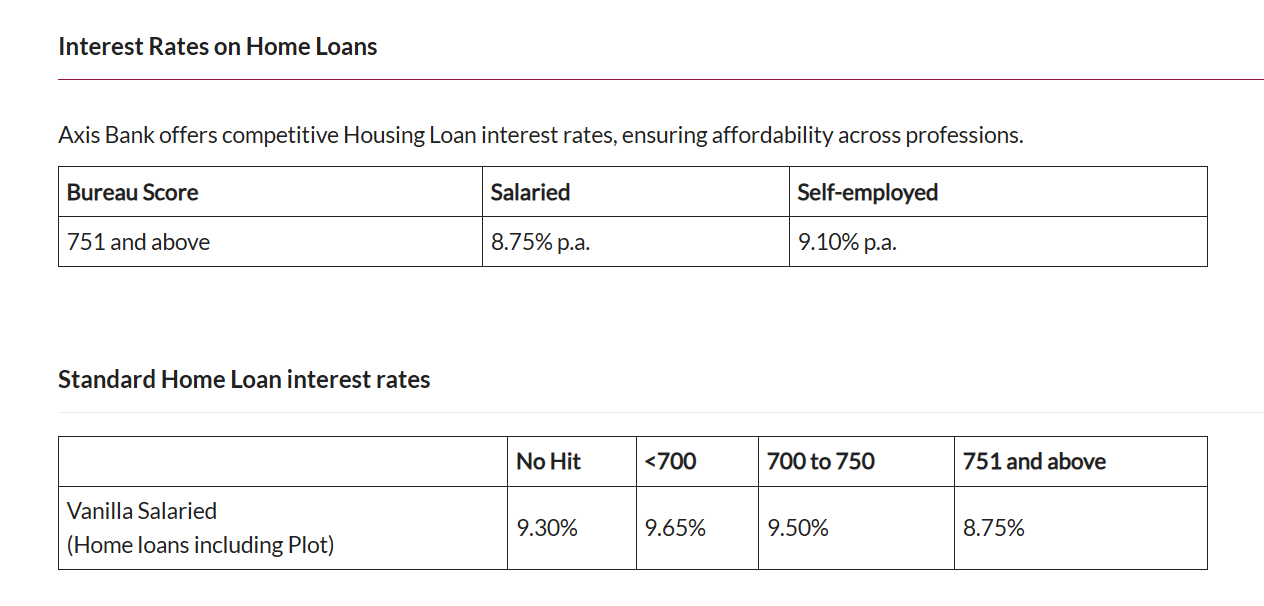

Axis Bank Home Loans Updated Interest Rates 2024

Axis Bank offers a wide range of home loans for general Home Loans to Shubh Arambh Home loans, Fast Forward Home Loans which provides quick disbursal of loan with minimum documentation requirements and EMI waiver facilities. Asha Home loans for affordable home buyers, Top up home loans, Super Saver home loans and many more.

Official site: https://www.axisbank.com/retail/loans/home-loan

Axis Bank Home Loan - Source : Axis Bank Official Page

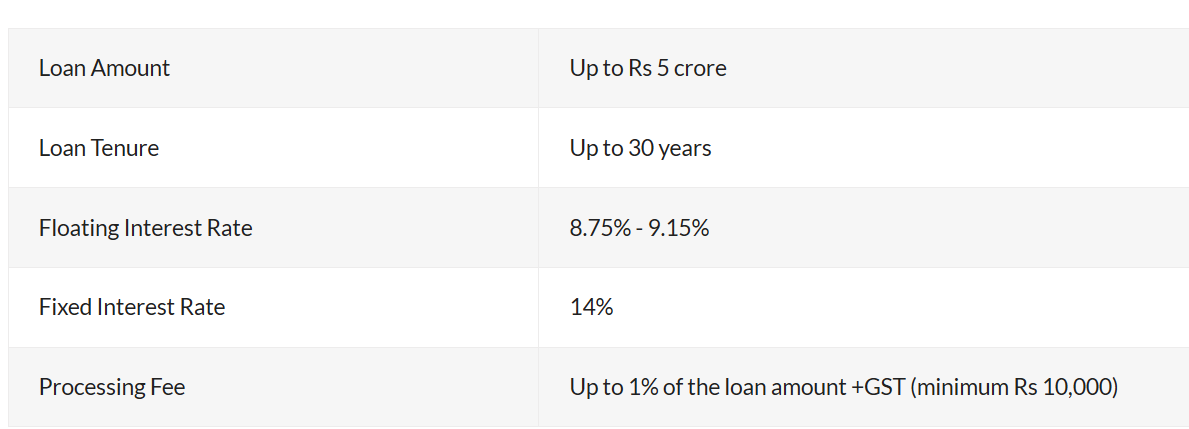

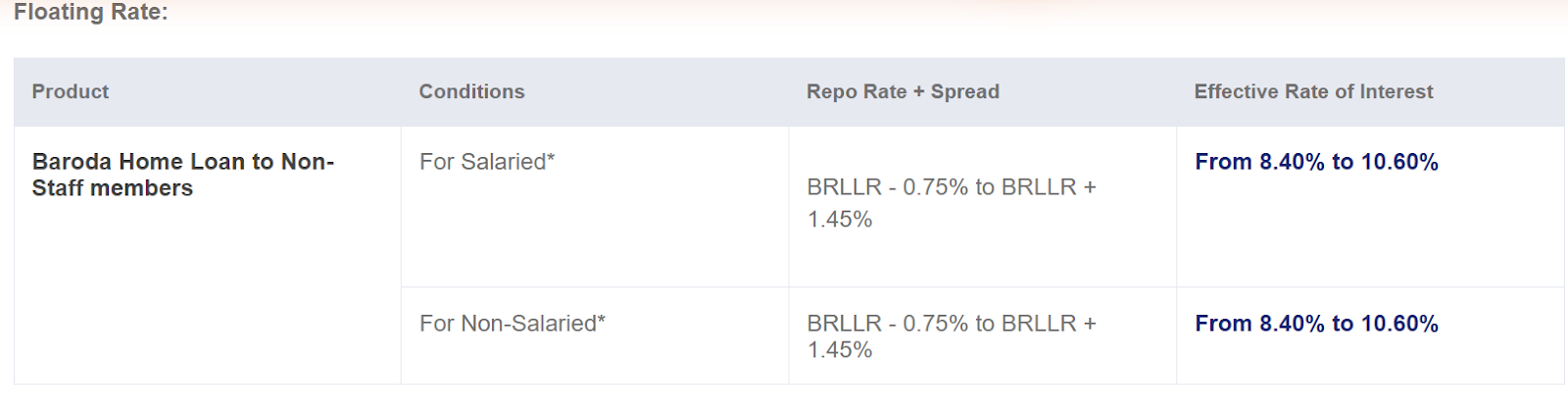

Bank of Baroda Home Loans Updated Interest Rates 2024

Bank of Baroda offers competitive home loan interest rates starting at 8.60% per annum as of January 2024, with a maximum loan tenure of up to 30 years for both salaried and self-employed individuals.

Special interest rates are available for women, senior citizens, and NRIs, catering to diverse applicant profiles. Eligibility criteria include meeting specific credit score requirements in line with Bank of Baroda's policies.

Additionally, the bank charges a processing fee of up to 0.35% of the loan amount, plus applicable taxes.

Benefits of Home Loans by Bank of Baroda

Low interest rates

Low processing charges

Higher Loan Amount

Interest charges on Daily Reducing Balance

Repayment up to 30 years

Moratorium period up to 36 months after the loan amount is disbursed.

Free Credit Card

Longer tenures

Easy Top Up Loan

Generally, the bank accepts mortgages of the constructed or purchased property as collateral. In some cases, collateral for home loans can be accepted in the form of insurance policies, government promissory notes, shares and debentures, gold ornaments and other property etc.

Maximum Loan Amount

Mumbai : Rs. 20 Crores

Hyderabad, New Delhi (including National Capital Region) and Bengaluru: Rs.7.50 Crore

Other Metros : Rs. 5.00 Crores

Urban Areas : Rs. 3.00 Crores

Semi-urban and Rural : Rs. 1.00 Crores

Chandigarh, Panchkula & Mohali:- Rs. 5 Crore

Bank of Baroda Interest Rates on Home Loan 2024

Floating Rate

Fixed Rate

Also Read: 5 Best Banks For Plot Loans in India : Interest Rate, Eligibility, Features

Advantages of Taking A Home Loan

The advantages of home loans include:

Financial Assistance: Home loans provide financial assistance to individuals who may not have the entire amount required to purchase a home upfront, making homeownership more accessible.

Tax Benefits: Home loan borrowers can avail tax benefits on both the principal amount and the interest paid, helping in reducing the overall tax liability.

Flexible Repayment Options: Home loans offer flexible repayment options, allowing borrowers to choose a tenure that suits their financial situation and repayment capacity.

Leverage Investment: Home loans allow individuals to leverage their investment by purchasing a property that may appreciate in value over time, potentially leading to long-term financial gains.

Ownership: One of the most significant advantages of a home loan is the opportunity to own a property, providing a sense of security and stability for the borrower and their family.

Also Read: How can Home Loan Save Taxes 2024

Conclusion

By carefully considering these factors, potential home loan borrowers can make informed decisions, choose the right lender, and select a home loan that aligns with their financial needs and goals.

In conclusion, choosing the right home loan can be a daunting task, especially with the numerous options available in the Indian market. However, by understanding the different types of home loans, such as fixed-rate, floating-rate, and affordable housing loans, and considering factors like interest rates, loan tenure, loan amount, tax benefits, and lender reputation, homebuyers can make informed decisions that align with their financial goals and needs.

Top lenders like SBI, HDFC Bank, ICICI Bank, Axis Bank, and Bank of Baroda offer competitive interest rates and flexible repayment options, catering to a wide range of borrowers. By carefully evaluating these options and considering the factors mentioned above, aspiring homeowners can secure the best home loan for their dream home.

explore further

Latest from Editorials

More from Publications

Resources

Dwello, for every home buyer, is a way to go from 'I feel' to 'I know', at no extra cost.