HRA is a crucial part of salary structuring, as it helps reduce taxable income while supporting employees in managing their housing costs. However, to claim tax benefits, individuals must provide proper rent receipts or rental agreements as proof of expense.

Home Interior Deals

Get Upto 25% off on modular home interior solutions with Livspace

HomeLane Offer

Beautiful Interiors, Delivered with the Peace of Mind You Need

Home

House Rent Allowance (HRA): Calculation, Tax Benefits & Exemptions

Understand House Rent Allowance (HRA) in India—eligibility, calculation, tax benefits under Section 10(13A), exemptions, and how to maximize deductions.

Avani Goswami

a year ago

Published Date: Apr 04, 2025

Updated Date: Apr 04, 2025

Table of Contents

- What is House Rent Allowance (HRA)?

- HRA Calculation: How is it Determined?

- HRA Exemption for Metro & Non-Metro Cities

- Tax Benefits of HRA Under Section 10(13A)

- How to Claim HRA Tax Exemption?

- HRA for Employees Living with Parents or in Own House

- HRA vs. Section 80GG: Which One to Claim?

- HRA Tax Exemption for Joint Rent Payments

- Common HRA Mistakes to Avoid

- Faq's

What is House Rent Allowance (HRA)?

House Rent Allowance (HRA) is a component of an employee's salary that is provided by the employer to cover rental expenses. It is particularly beneficial for salaried individuals living in rented accommodations, as it allows them to claim tax deductions under Section 10(13A) of the Income Tax Act, 1961. The amount of HRA received depends on several factors, including the employee's basic salary, the city of residence (metro or non-metro), and the rent paid.

HRA Calculation: How is it Determined?

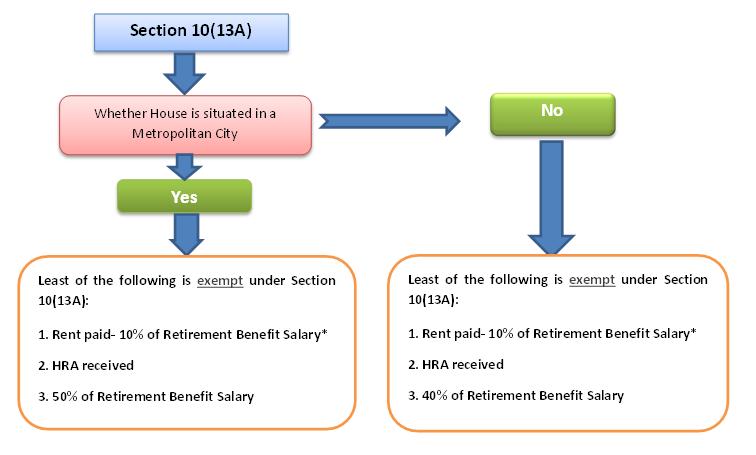

HRA exemption is calculated using three key factors:

The lowest of the following three amounts is exempt from tax:

- Actual HRA received from the employer

- 50% of basic salary + DA (for metro cities) / 40% (for non-metro cities)

- Actual rent paid minus 10% of basic salary + DA

Example Calculation

| Salary Components | Amount (₹) |

| Basic Salary | 50,000 |

| HRA Received | 20,000 |

| Rent Paid | 15,000 |

| City of Residence | Mumbai (Metro) |

Exempted HRA = Lowest of the following:

- HRA Received = ₹20,000

- 50% of Basic Salary (Metro City) = ₹50,000 × 50% = ₹25,000

- Rent Paid - 10% of Basic Salary = ₹15,000 - ₹5,000 = ₹10,000

Tax-free HRA = ₹10,000 per month (₹1,20,000 annually)

The remaining ₹10,000 per month is taxable

HRA Exemption for Metro & Non-Metro Cities

- 50% of Basic Salary is tax-free in metro cities (Mumbai, Delhi, Chennai, Kolkata).

- 40% of Basic Salary is tax-free in non-metro cities.

Here's the Metro vs. Non-Metro Cities for HRA Calculation in a table format:

| Metro Cities (50% of Basic Salary) | Non-Metro Cities (40% of Basic Salary) |

| Mumbai | Bengaluru |

| Delhi | Hyderabad |

| Chennai | Pune |

| Kolkata | Ahmedabad |

| Jaipur | |

| Lucknow | |

| Surat | |

| Indore | |

| Chandigarh | |

| Coimbatore | |

| Bhopal | |

| Kochi | |

| Patna | |

| Nagpur | |

| Visakhapatnam | |

| Guwahati | |

| Bhubaneswar | |

| Madurai | |

| Thiruvananthapuram | |

| Other cities not classified as metros |

Tax Benefits of HRA Under Section 10(13A)

- Reduces Taxable Income - Helps salaried individuals save tax on rental expenses.

- Higher Benefit for Metro Cities - Employees in metro cities get a higher 50% deduction.

- Allows Tax Deduction Alongside Home Loan - You can claim HRA + Home Loan Tax Benefits together.

- Applicable to Salaried Employees Only - Self-employed individuals cannot claim HRA but can deduct rent under Section 80GG.

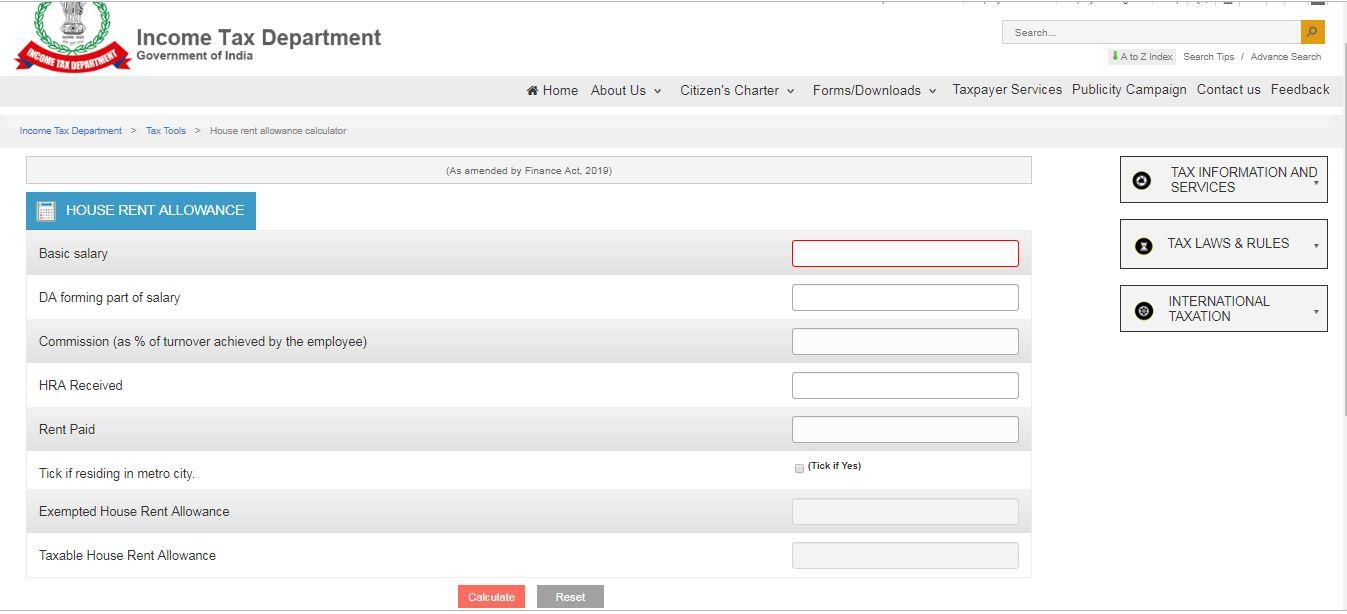

How to Claim HRA Tax Exemption?

To claim an HRA tax deduction, follow these steps:

- Submit Rent Receipts & Rental Agreement: Provide monthly rent receipts and a copy of the rental agreement to your employer.

- Landlord's PAN is Mandatory for Rent Above ₹1 Lakh Annually: If your annual rent exceeds ₹1,00,000, your employer will require the landlord's PAN.

- Declare HRA in Your ITR & Form 16: Include your HRA details in Form 16 while filing your Income Tax Return (ITR).

- Ensure Rent Payments are Made via Bank Transfer: Paying rent via cash may lead to rejection of the exemption claim.

- Avoid Fake Rent Receipts: Submitting false rent receipts can lead to tax penalties and scrutiny.

HRA for Employees Living with Parents or in Own House

1. Can I Pay Rent to My Parents and Claim HRA?

Yes, but you must:

- Pay rent via bank transfer or cheque.

- Have a rental agreement with your parents.

- Ensure your parents declare rental income in their ITR.

2. Can I Claim HRA If I Own a House?

- If you live in your own house, you cannot claim HRA.

- However, if you own a house in a different city and live in a rented house for work, you can claim both HRA and home loan benefits.

HRA vs. Section 80GG: Which One to Claim?

| Feature | HRA (Section 10(13A)) | Section 80GG |

| Eligibility | Salaried employees receiving HRA | Self-employed or salaried without HRA |

| Tax Benefit | Exemption on HRA received | Deduction up to ₹60,000/year |

| Conditions | Must live in rented accommodation | No owned house in the city |

HRA Tax Exemption for Joint Rent Payments

If two people share a rented house, both can split rent and claim HRA by:

- Having both names on the rental agreement.

- Paying rent via separate bank transactions.

- Keeping a clear record of rental payments.

Common HRA Mistakes to Avoid

- Submitting Fake Rent Receipts - Leads to tax scrutiny.

- Not Mentioning Landlord's PAN (If Rent > ₹1 Lakh Annually) - Can lead to claim rejection.

- Claiming Both HRA & Home Loan Without Proper Eligibility - Only valid if you own a house in another city.

- Not Keeping Proper Rent Payment Proofs - Tax authorities may demand transaction records.

explore further

Latest from Editorials

Exploring National Highway 83: The Ultimate Travel Guide from Coimbatore to NagapattinamExploring National Highway 113: A Scenic Journey to Hawa Camp & Kibithu in Arunachal PradeshExploring National Highway 79: The Ultimate Guide from Ulundurpettai to Salem, Tamil NaduGodrej Seeds and Genetics Ltd Drops ₹365 Crore on Three Premium Office Units in Mumbai’s VikhroliExploring National Highway 140: The Scenic Route from Chittoor to Tirupati, Andhra Pradesh

More from Publications

Resources

NEED HELP?

Get in touch with Dwello consultant for free consultation

+91

Enquire Now

Registered & Corporate Office

JM Financial Products Limited. 7th Floor, Cnergy, Appasaheb Marathe Marg, Prabhadevi, Mumbai - 400025

CIN:

U74140MH1984PLC033397

RERA NUMBERS

Maharashtra

A51900000277

Karnataka

PRM/KA/RERA/1251/309/AG/220521/002898

Delhi

DLRERA2022A0103

Haryana

RC/HARERA/GGM/1932/1527/2022/300

For any complaints please write to us at grievance@dwello.in

What is Dwello?

Dwello is a new way to buy home. In a world where facts are chosen to suit interpretations, our algorithms offer accurate recommendations by sifting through vast knowledge banks comprising real time market data and historical decisions of many home buyers, curated by industry experts.

Dwello, for every home buyer, is a way to go from 'I feel' to 'I know', at no extra cost.

Dwello, for every home buyer, is a way to go from 'I feel' to 'I know', at no extra cost.

© 2023 JM Financial Products Limited. All Rights Reserved.