Table of Contents

- What is Income Tax?

- What is Income Tax Return (ITR)?

- Income Tax Slab

- Income Tax and Real Estate

- Income Tax Portal (e-Filing)

- Key Services Available On The Income Tax Portal

- Information Needed For Income Tax e-Filing Portal

- Income Tax Portal: Registration Process

- Income Tax Portal: Login

- The Importance of Filing Income Tax Returns

- Income Tax Login via Internet Banking

- Understanding the Basics of House Property Tax

- Calculating Income From House Property

- Calculating GAV Of Let Out Property

- Tax on Rental Income

- Online Tax Payment Through e-Pay Tax

- Conclusion

- Faq's

What is Income Tax?

Income tax is a direct tax levied by the government on individuals, businesses, and other entities based on their income. In India, income tax is governed by the Income Tax Act, 1961, and is managed by the Central Board of Direct Taxes (CBDT). The income tax system is progressive, which means that higher-income earners are taxed at higher rates than those with lower incomes.

Income tax is calculated annually on the income earned during a specific financial year, which runs from April 1st to March 31st of the following year. Different sources of income, such as salary, business profits, capital gains, rental income, and interest earned, are considered while computing the total taxable income.

Various deductions, exemptions, and tax-saving investments allowed under the Income Tax Act can reduce the taxable income, thereby lowering the tax liability for taxpayers. The revenue generated from income tax plays a crucial role in funding government initiatives, public services, infrastructure development, and welfare programs. Income tax serves as a key source of revenue for the government and is essential for the functioning of a country's economy.

What is Income Tax Return (ITR)?

An Income Tax Return (ITR) is essentially a document or form that taxpayers in India submit to the Income Tax Department, providing details of their income earned during a specific financial year. This period typically spans from April 1st to March 31st of the following year. The purpose of filing an ITR is to declare one's income and tax liabilities accurately to the government.

In India, income tax is levied on individuals and entities based on the income they earn, and it is calculated as per the rules and tax slabs outlined by the Income Tax Department. These tax slabs range from nil tax for incomes below a certain threshold to a maximum of 30% for higher income brackets.

The income declared in an ITR can come from various sources such as salary, business profits, capital gains (from selling assets like property or investments), rental income, interest earned on savings or investments, and other sources as per the tax laws.

Filing an income tax return is mandatory for individuals and entities meeting certain income criteria, even if they don't have any tax liability after deductions and exemptions. This requirement applies to individuals who have bought or sold property, earned rental income, or engaged in any financial transactions that require tax reporting.

ITRs can be filed both online and offline, with the online method being more convenient and increasingly popular. To file online, taxpayers need to create an account and log in to the Income Tax Department's e-filing portal using their PAN (Permanent Account Number) and password.

One of the key benefits of filing an ITR is that it allows taxpayers to claim refunds if they have paid taxes over their actual tax liability. This often occurs when taxes are deducted at source (TDS) from income sources like salary or interest income, and the taxpayer is eligible for deductions or exemptions that reduce their overall tax liability.

Filing an Income Tax Return is not just a legal obligation but also a means for taxpayers to ensure compliance with tax laws, avail of tax benefits, and contribute to the country's revenue system responsibly.

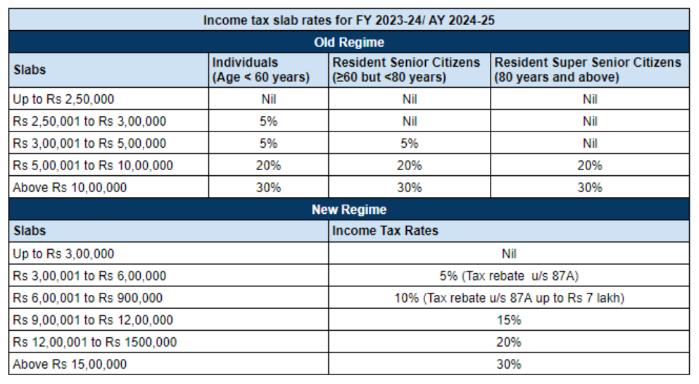

Income Tax Slab

Income tax in India is structured based on a slab system, which assigns different tax rates to various income ranges for individuals. As income levels rise, so do the corresponding tax rates. This system fosters fairness and progressivity in taxation, ensuring that those with higher incomes contribute proportionately more to the government's revenue.

The income tax slabs are subject to periodic revisions, often aligned with each fiscal year's budget. For the financial year 2023-24 (Assessment Year 2024-25), the applicable income tax slab rates are diverse and tailored for different categories of taxpayers. These rates outline the percentage of tax payable based on the income earned within specific brackets, thereby delineating the tax liability for individuals across income spectrums.

Income Tax Slab Rates

Income Tax Slab Rates

Image Source: Clear Tax

Income Tax and Real Estate

Taxability of income from real estate is an important aspect of income tax laws in India, affecting both residents and non-residents (NRIs). Here are the key scenarios where individuals need to pay income tax related to real estate:

Rental Property Income:

- Income earned from renting out a property is taxable and needs to be included in the taxpayer's income tax returns. This income falls under the purview of Section 24 of the Income Tax Act. Expenses related to the maintenance and upkeep of the property can often be deducted from this income, reducing the taxable amount.

Home Loan and Interest Deductions:

- If an individual has taken a home loan to purchase a house, they can claim deductions under various sections of the Income Tax Act. For instance, the interest paid on the home loan can be claimed as a deduction under Section 24. Additionally, principal repayments are eligible for deductions under Section 80C within specified limits.

Capital Gains on Property Sale:

- When a property is sold, any profit made on the sale is termed as capital gains and is subject to taxation. The tax treatment depends on whether it is a short-term capital gain (STCG) or a long-term capital gain (LTCG).

- Short-term capital gains arise when a property is held for less than 24 months (36 months for immovable property like land or buildings). For STCG, a flat tax rate of 15% applies.

- Long-term capital gains result from the sale of property held for more than the specified period. The tax rate for LTCG is determined based on indexation and the individual's applicable tax slab.

Tax Deduction at Source (TDS):

- In certain real estate transactions, such as property sales, TDS may be applicable. The buyer is required to deduct TDS at specified rates and deposit it with the government. The seller can then claim credit for this TDS while filing their income tax return.

Taxpayers involved in real estate transactions must understand these tax implications and comply with the Income Tax Act's provisions. Seeking guidance from tax professionals or using online resources provided by the Income Tax Department can help in ensuring accurate tax compliance and optimizing tax benefits where applicable.

Income Tax Portal (e-Filing)

The Income Tax Portal, also known as the Income Tax e-filing portal, is an online platform provided by the Income Tax Department of India to facilitate various tax-related activities for taxpayers. It serves as a centralized hub for taxpayers to manage their income tax filings, track refunds, access tax forms and statements, and engage with tax authorities for grievance resolution and compliance purposes.

Official Website: https://www.incometax.gov.in/iec/foportal/

Income Tax Portal

Income Tax Portal

Key Services Available On The Income Tax Portal

Submission of Income Tax Rectification Request:

- Taxpayers can rectify errors or discrepancies in their filed income tax returns through this service, ensuring accurate reporting of income and tax details.

e-Verify Returns:

- After filing tax returns online, taxpayers can electronically verify them using various methods provided by the portal, such as Aadhaar OTP, net banking, or electronic verification code (EVC).

Download Form 26AS:

- Form 26AS is a consolidated tax statement that provides details of tax credits, TDS (Tax Deducted at Source), and other financial transactions related to a taxpayer's PAN. The portal redirects to TRACES (TDS Reconciliation Analysis and Correction Enabling System) for Form 26AS download.

Submit Income Tax Grievance:

- Taxpayers can raise grievances related to income tax matters through the portal, seeking resolution or clarification on tax-related issues.

Generate Electronic Verification Code (EVC):

- EVC is a one-time password generated through the income tax portal, used for electronic verification of tax returns, requests, and other documents.

View Previous ITRs (Income Tax Returns):

- Taxpayers can access and view details of their previously filed income tax returns through the portal, facilitating record-keeping and reference for future filings.

View Form 15CA:

- Form 15CA is a declaration required for certain types of foreign remittances. Taxpayers can view and download this form from the portal as needed for specific transactions.

Check the Status of Complaints:

- Taxpayers can track the status of any complaints or grievances registered on the Income Tax e-filing portal, ensuring transparency and follow-up on reported issues.

Pre-validate Bank/Demat Account:

- Taxpayers can pre-validate their bank or demat accounts through the portal, which is often required for processing refunds, receiving tax credits, or completing financial transactions seamlessly.

|

Service Description |

Purpose |

|

Submission of Income Tax Rectification Request |

Rectify errors or discrepancies in filed returns |

|

e-Verify Returns |

Electronically verify filed tax returns |

|

Download Form 26AS |

Obtain consolidated tax statement and details |

|

Submit Income Tax Grievance |

Raise and resolve tax-related grievances |

|

Generate Electronic Verification Code (EVC) |

Generate one-time password for verification |

|

View Previous ITRs (Income Tax Returns) |

Access and review past filed tax returns |

|

View Form 15CA |

View and download Form 15CA for foreign remittances |

|

Check Status of Complaints |

Track status of complaints registered |

|

Pre-validate Bank/Demat Account |

Validate bank or demat accounts for transactions |

These services collectively enhance the user experience, streamline tax compliance processes, and provide necessary tools for effective tax management and grievance resolution.

Information Needed For Income Tax e-Filing Portal

To register on the Income Tax e-filing portal and complete the Income Tax login process, you need to provide accurate information for verification purposes. Here is a list of details required for Income Tax login:

- Email Address: You need a valid email address to receive notifications, updates, and communications from the Income Tax Department regarding your tax filings and other related matters.

- Address Proof (Current): You must provide a valid address proof to verify your current residential address. This could be in the form of a utility bill, Aadhaar card, passport, or any other government-issued document with your current address.

- Mobile Number: A registered mobile number is essential for receiving OTPs (One-Time Passwords) during the Income Tax login process, e-verification of tax returns, and other authentication purposes.

- PAN Number (Mandatory): Your PAN (Permanent Account Number) is a unique identifier issued by the Income Tax Department. It is mandatory for Income Tax login and is used to link your tax records, filings, and transactions to your PAN account.

Income Tax Portal: Registration Process

To register on the Income Tax login portal and gain access to tax-related services such as filing taxes for property transactions, rentals, or home income, follow these steps:

- Step 1: Visit the Income Tax Login portal at: https://www.incometax.gov.in/iec/foportal/

Income Tax Login Portal

Income Tax Login Portal

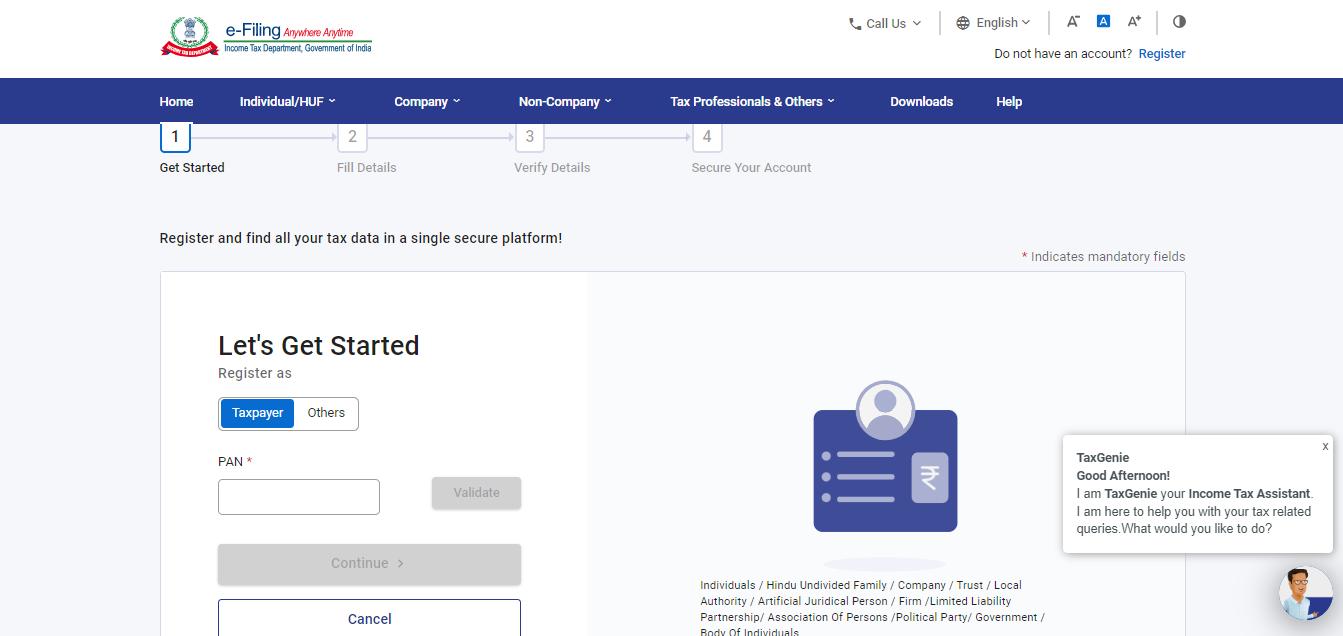

- Step 2: Click on the "Register" option displayed on the portal's homepage.

Registration Page

Registration Page

- Step 3: Choose the appropriate registration category, such as "Taxpayer" or "Others," based on your profile and requirements.

- Step 4: Enter your PAN number in the provided field and click on "Continue" to proceed with the registration process.

- Step 5: Fill in the required details such as password information, contact information (including a valid mobile number and email address), current residential address, and a secret question for security purposes.

- Step 6: Submit the registration form. Upon successful submission, the system will initiate a verification process.

- Step 7: You will receive a six-digit verification code on your registered mobile number and email address. If you are an NRI, an OTP (One-Time Password) will be sent to your registered email address.

- Step 8: Enter the verification code or OTP within 24 hours to complete the verification process. Failure to enter the code within the specified timeframe will require restarting the registration process.

Once the verification is completed successfully, you will gain access to your Income Tax login account, allowing you to file taxes, manage tax-related transactions, and utilize various services offered by the Income Tax Department online.

Income Tax Portal: Login

To log in to the Income Tax e-filing portal and manage taxes related to capital gains or other income, follow these steps:

- Step 1: Visit the Income Tax e-filing login portal and enter your login username or user ID.

- Step 2: You will be redirected to the Income Tax Login page.

IT Portal Login Page

IT Portal Login Page

- Step 3: On the login page, provide your PAN (Permanent Account Number) and the password you selected during the Income Tax e-filing registration process. Enter the Captcha code as displayed on the screen for security verification.

- Step 4: After entering the required details, click on the "Login" button to access your Income Tax e-filing account.

Upon successful login, you will be able to view and manage your tax-related information, file income tax returns, pay taxes, and perform various tasks related to capital gains or other income sources as per the Income Tax Department's guidelines.

The Importance of Filing Income Tax Returns

Filing an income tax return is indeed mandatory in India if your income exceeds the threshold exempt from income tax, which varies based on the individual's age and income sources. The Income Tax Act stipulates these thresholds and outlines the process for filing tax returns. Failure to file an income tax return when required can have several implications, both financial and legal.

Financial Implications:

- Tax Compliance: Non-filing of income tax returns can lead to non-compliance with tax laws, which may result in penalties and interest on unpaid taxes.

- Tax Refunds: If you are eligible for tax refunds due to excess tax deductions or other reasons, not filing a return means you won't receive these refunds promptly.

- Impact on Loans: Banks and financial institutions often require income tax returns as proof of income for various loan applications, such as home loans, personal loans, or car loans. Non-submission of tax returns may affect your loan approval process or terms.

- Visa and Immigration: For visa and immigration processes, especially for NRIs (Non-Resident Indians) or individuals applying for work or study visas abroad, income tax returns are often required as part of the documentation to demonstrate financial stability and compliance with tax laws.

Legal Implications:

- Penalties: The Income Tax Department can levy penalties for non-filing or delayed filing of income tax returns. These penalties can vary based on the duration of non-compliance and the amount of tax liability.

- Scrutiny and Audits: Non-filing of returns might also attract scrutiny from tax authorities, leading to audits and inquiries regarding your financial transactions and income sources.

Compliance and Documentation:

- Filing income tax returns ensure that you are compliant with tax regulations and fulfill your civic responsibility.

- It also serves as documentary proof of your income, tax deductions, investments, and financial transactions, which can be useful in various financial and legal contexts.

Income Tax Login via Internet Banking

Income taxpayers in India can conveniently access the Income Tax filing login portal through internet banking services offered by major banks. However, this facility is accessible only to individuals who have updated their PAN card details with their respective banks. Here is a step-by-step guide to login to the Income Tax portal using internet banking:

- Step 1: Visit the e-filing login portal through your bank's internet banking page. Look for the section that provides access to Income Tax login services. You will find a list of banks that offer this facility.

- Step 2: Choose your bank from the list and click on its name. This action will redirect you to your bank's Internet banking page.

- Step 3: On the bank's Internet banking page, log in using your net banking ID and password. Once successfully logged in, you will gain access to various services provided by the bank.

From there, you can navigate to the Income Tax e-filing section or use any specific links provided by your bank to directly access the Income Tax portal. This method streamlines the login process and allows taxpayers to manage their tax-related activities seamlessly through their bank's Internet banking platform.

Understanding the Basics of House Property Tax

House property taxation encompasses various types of properties under the Income Tax Act, irrespective of whether they are used for residential or commercial purposes. Here's a breakdown of the basics of house property tax:

Definition of House Property:

- A house property can include a residential home, office space, a shop, a building, or land attached to a building (such as a parking lot). The Income Tax Act does not differentiate between commercial and residential properties; they are all taxed under the head 'income from house property' in the income tax return.

Ownership for Taxation:

- For income tax purposes, the owner of a property is considered its legal owner, capable of exercising ownership rights directly, not on behalf of someone else.

Self-Occupied House Property:

- A self-occupied house is one used for the taxpayer's residential purposes, including family members like parents, spouse, and children. Even a vacant property can be considered self-occupied for tax purposes.

- Until FY 2019-20, if taxpayer-owned multiple self-occupied properties, only one was considered self-occupied, and the others were treated as let out. However, from FY 2019-20 onwards, taxpayers can now treat two properties as self-occupied for tax benefits.

Let-Out House Property:

- A property that is rented out, either wholly or partially, during the year is categorized as a let-out house property for income tax purposes.

Inherited Property:

- Inherited properties can be self-occupied or let out based on their usage, similar to properties acquired through purchase.

Calculating Income From House Property

Here's a step-by-step guide on how to compute income from a house property for income tax purposes:

Determine Gross Annual Value (GAV):

- For a self-occupied house, the GAV is considered zero since no rent is collected.

- For a let-out property, the GAV is the actual rent received or receivable for the property during the financial year.

Reduce Property Tax (Municipal Taxes):

- Property tax paid during the previous year is allowed as a deduction from the GAV to arrive at the Net Annual Value (NAV).

Calculate Net Annual Value (NAV):

- NAV = Gross Annual Value (GAV) - Property Tax

Apply Standard Deduction:

- Deduct 30% of the NAV towards standard deduction under Section 24 of the Income Tax Act. This deduction covers expenses like repairs, maintenance, insurance, etc., and is capped at 30% of the NAV.

Deduct Home Loan Interest:

- Deduction under Section 24 is also available for interest paid during the year on a housing loan taken for the property. The interest deduction is subject to certain conditions and limits.

Determine Income/Loss from House Property:

- The resulting value after deducting standard deduction and home loan interest is your income from house property if it's positive, or loss if it's negative.

Adjustment of Loss from House Property:

- If there is a loss from house property, it can be adjusted against income from other heads, subject to a maximum limit of 2 lakh rupees in a year.

- Any loss exceeding 2 lakh rupees can be carried forward for up to 8 years and set off against income under the head "Income from House Property" in subsequent years.

Note:

For let-out properties, the GAV is based on the actual rent received or the municipal value, whichever is higher. This ensures that the rental value is at least equal to the reasonable rent determined by the municipality.

Calculating GAV Of Let Out Property

Suppose Rajesh owns a property that is let out for the entire year. Here are the relevant details:

- Municipal Value: Rs. 1,00,000

- Fair Rent: Rs. 1,20,000

- Standard Rent: Rs. 1,10,000

- Actual Rent Received: Rs. 1,15,000

To compute the GAV, we follow these steps:

Expected Rent (ER):

- ER = Higher of (Fair Rent, Municipal Value) but restricted to Standard Rent

- ER = Higher of (Rs. 1,20,000, Rs. 1,00,000) but restricted to Rs. 1,10,000 (Standard Rent)

- ER = Rs. 1,10,000

GAV Calculation:

- Since the property is let out for the whole year, GAV will be the higher of ER and Actual Rent Received.

- GAV = Higher of (ER, Actual Rent) = Higher of (Rs. 1,10,000, Rs. 1,15,000) = Rs. 1,15,000

Therefore, the Gross Annual Value (GAV) of Rajesh's let-out property is Rs. 1,15,000 for the relevant financial year.

This example illustrates how to calculate GAV for a let-out property using the expected rent and actual rent received, ensuring compliance with income tax regulations regarding property taxation.

Tax on Rental Income

Let's consider the following details for the rental property:

- Monthly rent of the apartment: Rs. 25,000

- Property tax paid during the year: Rs. 20,000

- Interest paid on a home loan for the property: Rs. 40,000

- Standard deduction rate: 30%

Now, let's calculate the taxable income step by step:

Calculation of Gross Annual Value (GAV):

- Monthly Rent: Rs. 25,000

- GAV = Monthly Rent x 12 months = Rs. 3,00,000

Deduction of Property Tax from GAV:

- Property Tax Paid: Rs. 20,000

- Net Annual Value (NAV) = GAV - Property Tax = Rs. 3,00,000 - Rs. 20,000 = Rs. 2,80,000

Standard Deduction:

- Standard Deduction (30% of NAV) = 30% x Rs. 2,80,000 = Rs. 84,000

Interest Paid on Home Loan:

- Interest Paid on Home Loan: Rs. 40,000

Taxable Income Calculation:

- Taxable Income = NAV - Standard Deduction - Interest Paid on Home Loan

- Taxable Income = Rs. 2,80,000 - Rs. 84,000 - Rs. 40,000 = Rs. 1,56,000

So, the taxable income from the rental property for the given year is Rs. 1,56,000.

To pay the tax on this rental income, follow the steps

- Go to the Income Tax e-filing portal and log in.

- Enter personal details and income sources, including rental income, property taxes, and home loan interest.

- Upload relevant documents such as Form 16 or enter details manually.

- Enter TDS information and any other sources of income.

- Review and submit the information to calculate your tax liability based on the taxable income.

This example helps us understand the process of calculating taxable income from rental property and filing income tax accordingly.

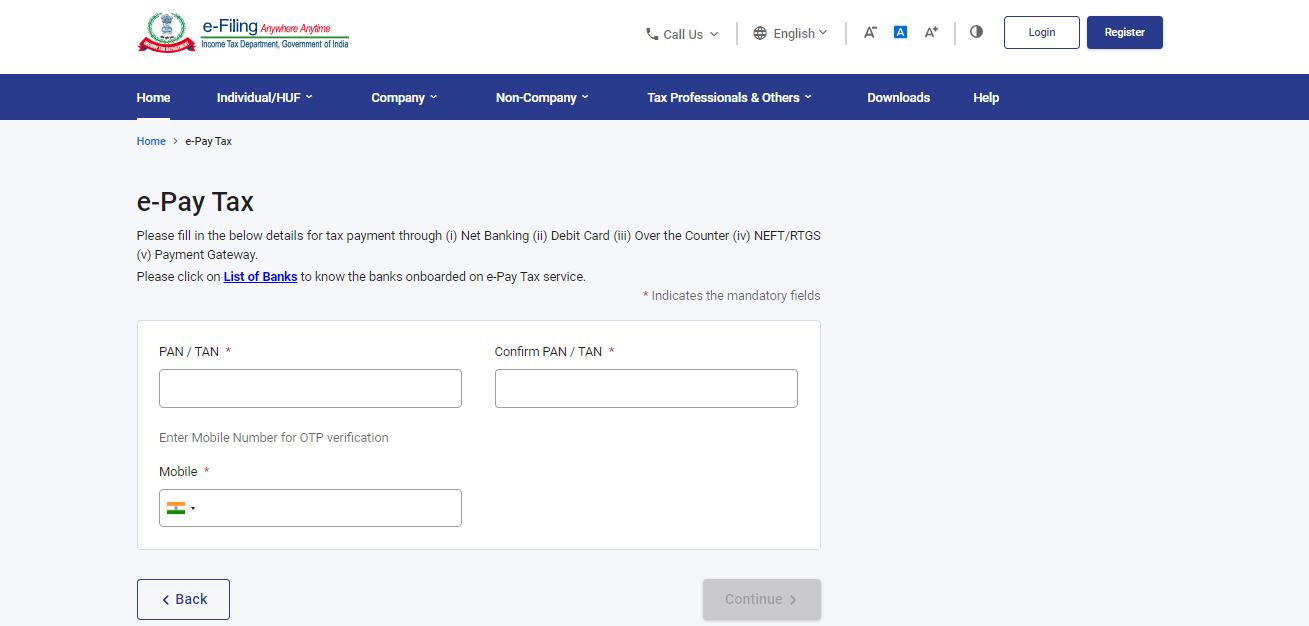

Online Tax Payment Through e-Pay Tax

Step 1: Access the 'e-Pay Tax' Section

- Visit the Income Tax Portal.

- Locate the 'Quick Links' section on the homepage.

- Click on 'e-Pay Tax' or use the search option to find it.

e-Pay Tax

e-Pay Tax

Step 2: Provide PAN/TAN and Mobile Number

- Enter your PAN and confirm it.

- Input your mobile number and click 'Continue'.

- Verify the 6-digit OTP received on your mobile.

Step 3: Selecting Assessment Year and Payment Type

- Choose 'Income Tax' from the payment options and click 'Proceed'.

- From the dropdown, select the correct Assessment Year (e.g., 2024-25).

- Under 'Type of Payment', choose 'Self-Assessment Tax (300)' and continue.

Step 4: Entering Tax Payment Details

- Fill in the payment amounts accurately as per your tax liability.

- Refer to the pre-filled challan on the portal for necessary amounts.

Step 5: Choosing Payment Method

- Select your preferred payment method (internet banking, debit/credit card, RTGS/NEFT, UPI).

- Choose the bank and click 'Continue' to proceed to payment.

Step 6: Verifying Payment Information

- Preview the challan details and ensure accuracy.

- Click 'Pay Now' to initiate the payment process.

Step 7: Submitting the Payment

- Agree to the Terms and Conditions by checking the box.

- Click 'Submit To Bank' to complete the payment process.

Step 8: Receiving Payment Confirmation

- You will receive a confirmation of the successful tax payment.

- Download the challan for reference and future filings.

Step 9: Updating Tax Payment Details

- After payment, update the payment information on the portal or tax filing platform (if applicable).

- Either upload the challan or manually input the payment details.

Conclusion

To conclude, navigating the intricacies of income tax with rental income involves understanding various calculations and deductions, such as Gross Annual Value (GAV), Net Annual Value (NAV), standard deductions, and interest on home loans. Utilizing online platforms like the Income Tax e-filing portal streamlines this process and ensures accurate tax reporting. Moreover, comprehending house property taxation nuances, including the distinction between self-occupied and let-out properties, is essential for taxpayers. By fulfilling tax obligations responsibly and leveraging digital tools, taxpayers contribute not only to their own financial compliance but also to the smooth functioning of the nation's revenue system.

explore further

Latest from Editorials

More from Publications

Resources

Dwello, for every home buyer, is a way to go from 'I feel' to 'I know', at no extra cost.