Table of Contents

- Introduction

- Understand Why Your Loan Was Rejected

- Review and Correct Your Credit Report

- Improve Your Financial Health

- Fix Errors and Strengthen Future Applications

- Explore Alternative Lenders or Loan Products

- Strengthen Your Credit Profile

- Reapply Strategically

- Conclusion

- Faq's

Introduction

Facing a loan rejection can feel like a setback, but it's not the end of your financial journey. Loan applications are often declined due to various reasons, including credit score issues, insufficient income, or incomplete documentation. The key to recovering from rejection is understanding the reasons behind it and taking the right steps to improve your eligibility. In this guide, we'll outline what you should do after your loan application is denied and how to increase your chances of approval in the future.

Understand Why Your Loan Was Rejected

The first and most crucial step is to determine the exact reasons behind the rejection. Lenders are legally obligated to provide a rejection notice, which typically outlines the specific issues. Common reasons include:

- Low Credit Score: Indicates that your creditworthiness isn't up to the lender's standards.

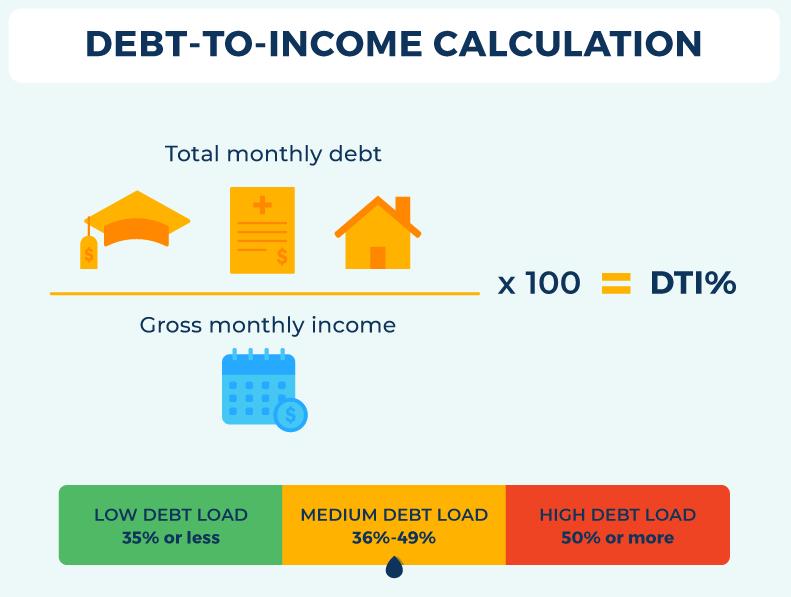

- High Debt-to-Income Ratio (DTI): Too much of your income is already committed to existing debts.

- Insufficient Income: Your income may not meet the lender's requirements for the requested loan amount.

- Incomplete Documentation: Missing or inaccurate paperwork can lead to immediate rejection.

Take the time to contact the lender if you need more clarity. A clear understanding of their decision will help you take targeted action.

Review and Correct Your Credit Report

Your credit report plays a significant role in loan approvals, so it's essential to assess it for errors or inaccuracies. Steps include:

- Obtain a Free Credit Report: Platforms like CIBIL, Equifax, or Experian offer free annual credit reports.

- Look for Errors: Check for outdated information, fraudulent accounts, or incorrect balances.

- Dispute Inaccuracies: Report errors to the credit bureau with supporting documents to have them corrected.

- Identify Problem Areas: Late payments, high credit utilization, or defaulted accounts are red flags. Work on addressing these issues.

Improve Your Financial Health

Lenders want assurance that you're financially stable and capable of repaying the loan. To improve your standing:

- Pay Down Existing Debt: Lowering your DTI ratio makes you a more attractive borrower. Focus on clearing high-interest debts first.

- Avoid New Credit: Applying for additional credit lines can make you appear financially overextended.

- Build an Emergency Fund: A savings cushion shows lenders that you're prepared for unexpected financial challenges.

- Increase Your Income: Explore side gigs, part-time work, or freelancing to enhance your monthly earnings.

Fix Errors and Strengthen Future Applications

Loan rejections can sometimes result from simple mistakes or incomplete applications. To avoid this in the future:

- Double-Check Documentation: Ensure all required forms, proofs of income, and identification are included and accurate.

- Provide Strong References: If applicable, include references or guarantors to strengthen your application.

- Clearly State the Purpose: Highlighting how the loan will be used (e.g., for education, home renovation) can make your application more compelling.

Explore Alternative Lenders or Loan Products

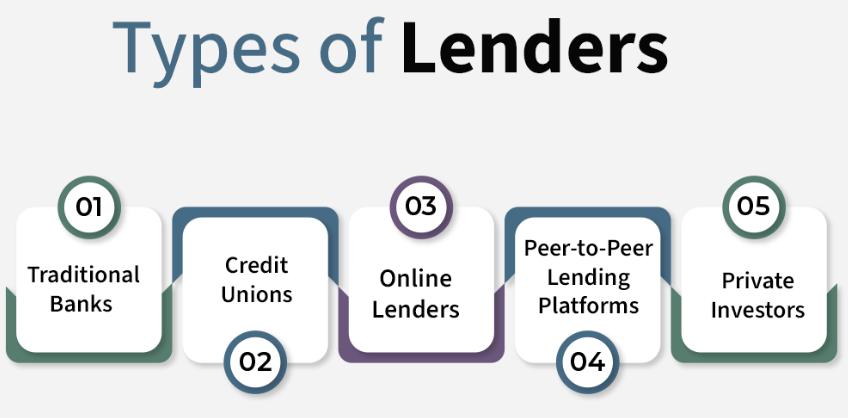

If one lender rejects your application, others may have more flexible terms. Options to consider:

- Credit Unions: These institutions often have lower eligibility criteria and better customer-focused policies.

- Peer-to-Peer Lending: Online platforms connect borrowers with individual lenders and may offer more relaxed requirements.

- Secured Loans: Offering collateral like a car or property can reduce the lender's risk and increase your chances of approval.

- Specialized Loans: Some lenders cater to individuals with low credit scores or specific financial situations, like credit-builder loans.

However, be cautious not to apply to multiple lenders at once. Each application can trigger a hard inquiry, which may temporarily lower your credit score.

Strengthen Your Credit Profile

Improving your credit score is a long-term strategy but essential for securing loans at better terms. Key actions include:

- Timely Payments: Always pay your credit card bills and EMIs on or before the due date.

- Lower Credit Utilization: Aim to use less than 30% of your available credit limit.

- Add Positive Credit History: Consider applying for a secured credit card or a small credit-builder loan and make consistent payments to demonstrate reliability.

Reapply Strategically

When you're ready to apply again, be smart about the process:

- Address the Previous Issues: Fix the specific reasons for your earlier rejection.

- Choose the Right Loan Amount: Reassess your borrowing needs and apply for an amount you can comfortably repay.

- Opt for Pre-Approval: Many lenders offer pre-approval services that give you an idea of your eligibility without affecting your credit score.

- Wait Until Financial Improvements Are Reflected: Give your credit score and financial health time to show positive changes before applying again.

Conclusion

A loan rejection doesn't have to be the end of your plans. By understanding the reasons behind the rejection, improving your financial health, and exploring alternative options, you can enhance your chances of approval the next time. Remember, patience and persistence are key to overcoming financial hurdles. With the right approach, you'll be on your way to securing the loan you need.

explore further

Latest from Did you know?

More from Interactions

Resources

Dwello, for every home buyer, is a way to go from 'I feel' to 'I know', at no extra cost.