Table of Contents

- Introduction

- SARFAESI Act

- Pros of Buying a Property Through a Bank Auction

- Cons of Buying a Property Through a Bank Auction

- Step-by-Step Guide to Buying a Property in a Bank Auction

- Conclusion

- Faq's

Introduction

Bank auctions are a popular way to purchase properties at prices lower than market value. When a borrower fails to repay a home loan, the bank seizes the property and auctions it to recover the outstanding dues. This process, conducted under the SARFAESI Act (Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act), ensures transparency and provides an opportunity for buyers to acquire real estate at competitive rates. Many investors and homebuyers are drawn to bank auctions due to the potential for high returns and affordability. However, buying an auctioned property comes with its own set of challenges. The process can be complex, involving strict payment deadlines, legal due diligence, and potential liabilities such as pending dues or existing occupants. Unlike regular property purchases, where a buyer has time to inspect and negotiate, bank auctions follow rigid timelines, requiring quick decision-making.

Property Auctions

Property Auctions

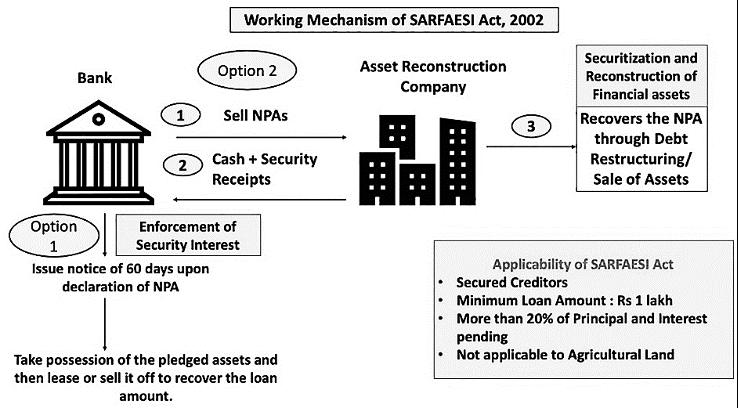

SARFAESI Act

The SARFAESI Act (Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002) is applicable in India. It allows banks and financial institutions to seize and auction properties when borrowers default on loans, without needing court intervention.

The SARFAESI Act is mainly used for:

- Recovering non-performing assets (NPAs) from defaulting borrowers.

- Empowering banks to auction secured properties (like homes and commercial buildings).

- Speeding up loan recovery without long legal battles in civil courts.

However, this law does not apply to:

- Agricultural land (cannot be seized under this act).

- Small loans (less than ₹1 lakh).

- Unsecured loans (since there is no collateral to auction).

SARFAESI Act (Process)

SARFAESI Act (Process)

Pros of Buying a Property Through a Bank Auction

- Lower Price than Market Value: One of the biggest advantages of buying a bank auction property is the cost. Since banks auction properties to recover unpaid loans, they often set the reserve price lower than the market rate, making it a great deal for buyers and investors.

- Transparent Process: Bank auctions follow a structured process under the SARFAESI Act, ensuring a fair and open bidding system. The auction details, including the reserve price, outstanding dues, and legal status, are publicly available, reducing the risk of hidden surprises.

- No Brokerage Fees: Unlike regular property purchases that involve brokers or real estate agents, buying directly from a bank means zero commission costs, making it more affordable.

- Immediate Transfer of Ownership: Once the winning bidder completes the payment, the bank issues a Sale Certificate, ensuring a relatively quick ownership transfer without the hassles of traditional property negotiations.

- Good Investment Potential: Properties bought at auctions often appreciate in value over time. Investors who conduct proper due diligence can make a high return on investment (ROI) by reselling or renting the property.

Cons of Buying a Property Through a Bank Auction

- Limited Property Inspection: Unlike regular home purchases, where buyers can inspect the property thoroughly, bank auctions may restrict physical visits, making it hard to assess its actual condition. Hidden damages or structural issues may lead to extra repair costs.

- Pending Dues and Liabilities: Some auctioned properties come with unpaid property tax, electricity bills, or society maintenance fees that the new owner must clear. Banks auction properties "as-is," meaning these liabilities become the buyer's responsibility.

- Legal Risks and Encumbrances: Some properties may have legal disputes, ongoing litigation, or claims from third parties, such as tenants refusing to vacate. Buyers must conduct a thorough legal check before bidding.

- Strict Payment Deadlines: Winning an auction does not mean instant ownership. The buyer must pay a significant amount (25% of the price) immediately and settle the full payment within a set time (typically 15-30 days). Failure to meet deadlines results in forfeiture of the Earnest Money Deposit (EMD).

- No Home Loan Availability Before Purchase: Unlike regular property transactions where buyers can apply for a loan beforehand, banks require full payment first before they transfer ownership. Buyers need liquidity or must arrange a loan quickly.

Step-by-Step Guide to Buying a Property in a Bank Auction

1. Research and Identify Suitable Auctions: Banks publish auction notices in newspapers, official websites, and government auction portals. These listings provide key details such as property location, reserve price, outstanding dues, and auction date. Prospective buyers should regularly check these sources to find properties that match their budget and requirements.

2. Verify Property Details and Legal Status: Before participating in the auction, it's essential to conduct a legal verification of the property. Check for any pending litigation, encroachments, unpaid dues (property tax, society maintenance, electricity bills), and ownership history. Engaging a property lawyer for a title check ensures there are no hidden legal complications.

3. Visit the Property (If Possible): Although some bank auctions restrict physical inspections, visiting the site can provide a clearer picture of the property's condition and surrounding locality. If direct inspection is not permitted, try gathering information from neighbors or local authorities.

4. Register for the Auction and Pay the EMD: To participate in the auction, buyers must register on the designated bank or auction portal and submit an Earnest Money Deposit (EMD), typically 10-15% of the reserve price. The deposit amount is refundable if the bidder does not win the auction.

5. Participate in the Bidding Process: The auction takes place either online or offline, where registered participants place bids above the reserve price. The highest bidder wins the property. Ensure you set a maximum bid limit to avoid overpaying beyond your budget.

6. Payment and Documentation: The winning bidder must pay a certain percentage of the amount (usually 25%) immediately, while the remaining balance must be cleared within a stipulated period (typically 15 to 30 days). Failure to pay within the deadline may result in the forfeiture of the EMD and cancellation of the sale.

7. Obtain the Sale Certificate and Property Possession: Once full payment is made, the bank issues a Sale Certificate, which must be registered at the sub-registrar's office. The buyer is responsible for paying stamp duty and registration charges. After registration, possession is handed over unless there are pending eviction proceedings.

8. Settle Any Pending Dues and Transfer Ownership: Check for outstanding charges like property tax, society maintenance fees, and utility bills. Once all dues are cleared, apply for a name transfer in municipal records to establish legal ownership.

Conclusion

Buying a bank auction property in India can be a great investment opportunity if done carefully. While the potential for discounted prices and clear ownership exists, risks such as legal issues, additional costs, and strict payment terms should not be ignored. Conducting due diligence, verifying legal documents, and consulting a property lawyer can help buyers make a secure and profitable purchase.

explore further

Latest from Home Buying Tips

More from Recommendations

Resources

Dwello, for every home buyer, is a way to go from 'I feel' to 'I know', at no extra cost.