Table of Contents

- Introduction

- What is a Home Loan Top-Up and How Does it Work?

- Eligibility Criteria for Home Loan Top-Up

- Benefits of a Home Loan Top-Up

- Taxation on Home Loan Top-Up Post 2025 Budget

- Conclusion

- Faq's

Introduction

A home loan top-up is an additional loan that borrowers can avail on their existing home loan. It is an excellent financial tool for those who need extra funds for home renovations, education, medical expenses, or even debt consolidation. Since it is secured against the property, the interest rates are usually lower than personal loans. In this guide, we will discuss the eligibility criteria, benefits, and tax implications of a home loan top-up.

Types Of Home Loans

Types Of Home Loans

What is a Home Loan Top-Up and How Does it Work?

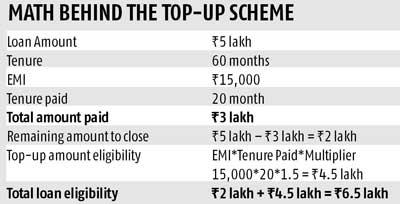

A home loan top-up is an extension of your existing home loan, allowing you to borrow additional funds without applying for a separate loan. The additional amount is disbursed based on your repayment track record and outstanding loan balance.

How It Works:

- You must have an existing home loan with a good repayment history.

- The lender evaluates your financial stability and outstanding balance.

- If eligible, you receive an additional loan amount at home loan interest rates.

- The repayment tenure is usually the same as the existing loan or can be adjusted per lender guidelines.

Tenure Range Of Home Loans

Tenure Range Of Home Loans

Eligibility Criteria for Home Loan Top-Up

To qualify for a home loan top-up, borrowers typically need to meet the following criteria:

- Existing Home Loan Holder: Must have an active home loan with the lender.

- Good Repayment Record: No history of missed EMIs or defaults.

- Loan Tenure: Should have completed a minimum repayment period as per lender policy.

- Sufficient Home Equity: The outstanding loan amount should not exceed a certain percentage of the property's value.

- Stable Income & Credit Score: A good credit history and stable income are essential for approval.

Benefits of a Home Loan Top-Up

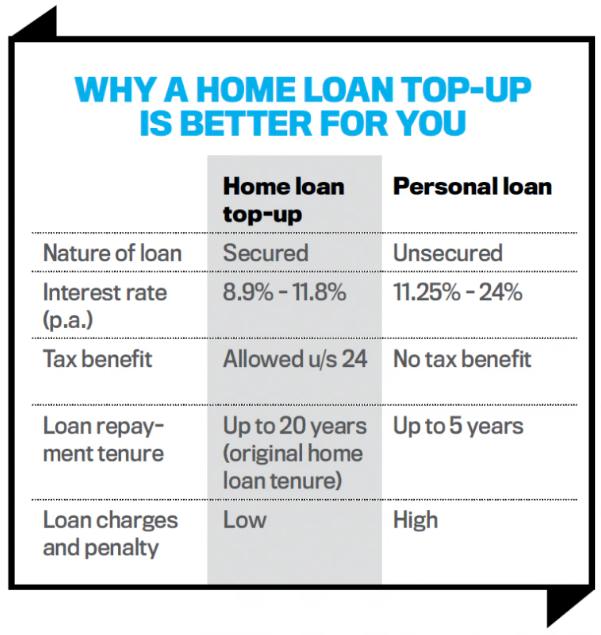

- Lower Interest Rates: Top-up loans typically have interest rates similar to or slightly higher than existing home loan rates, making them more affordable compared to personal loans, which often come with higher rates.

- Extended Loan Tenure: These loans can be aligned with your existing home loan tenure, offering a longer repayment period and reducing the burden of higher EMIs.

- Simplified Processing: Since you're an existing customer with a repayment history, the documentation and approval process for a top-up loan is generally quicker and more straightforward.

- Flexible Utilization: The funds from a top-up loan can be used for various purposes, such as home renovation, education, medical expenses, or other personal needs, providing flexibility to the borrower.

- Potential Tax Benefits: If the top-up loan is used for home renovation, construction, or repairs, you may be eligible for tax deductions on the interest paid, subject to specific conditions under the Income Tax Act.

Taxation on Home Loan Top-Up Post 2025 Budget

As per the 2025 Union Budget in India, there have been discussions about extending tax benefits to individuals opting for the new tax regime, including potential deductions on home loan interest. However, as of now, these benefits are primarily available under the old tax regime.

Under the Old Tax Regime:

-

Interest Deduction: You can claim a deduction of up to ₹2 lakh per annum on the interest paid for a self-occupied property. For let-out properties, there's no upper limit on the interest deduction.

Principal Repayment: Repayment of the principal amount qualifies for a deduction under Section 80C, subject to the overall limit of ₹1.5 lakh.

Under the New Tax Regime:

Currently, the new tax regime does not offer deductions for home loan interest or principal repayments. However, there are ongoing discussions and expectations that future budgets may introduce such benefits to make the new regime more attractive.

Important Considerations:

-

Usage of Funds: To avail tax benefits on a top-up loan, the borrowed amount must be used for the acquisition, construction, repair, or renovation of a residential property.

-

Documentation: Maintain proper records and proof of expenses to substantiate your claims during tax assessments.

It's advisable to consult with a tax professional or financial advisor to understand the implications based on your individual circumstances and to stay updated with any changes in tax laws.

Conclusion

A home loan top-up is a convenient financial solution for homeowners needing extra funds at affordable rates. It provides flexibility, lower interest costs, and tax-saving opportunities, making it an ideal alternative to personal loans. If you have an ongoing home loan with a good repayment history, a top-up loan can be a smart way to manage additional expenses.

explore further

Latest from Home Buying Tips

More from Recommendations

Resources

Dwello, for every home buyer, is a way to go from 'I feel' to 'I know', at no extra cost.