Table of Contents

- Introduction

- How to Save Interest on Home Loan

- Conclusion

- Faq's

Introduction

A home loan is often the most significant financial commitment of a lifetime, but that doesn't mean it has to drain your resources. By adopting smart strategies, you can significantly reduce the interest paid on your home loan, saving lakhs over the loan tenure. Whether you're considering prepayments, opting for repo-rate-linked loans, or switching lenders, understanding these methods can ease your financial burden. This article focuses on proven, actionable strategies to minimize your home loan interest, helping you stay ahead in your financial journey.

How to Save Interest on Home Loan

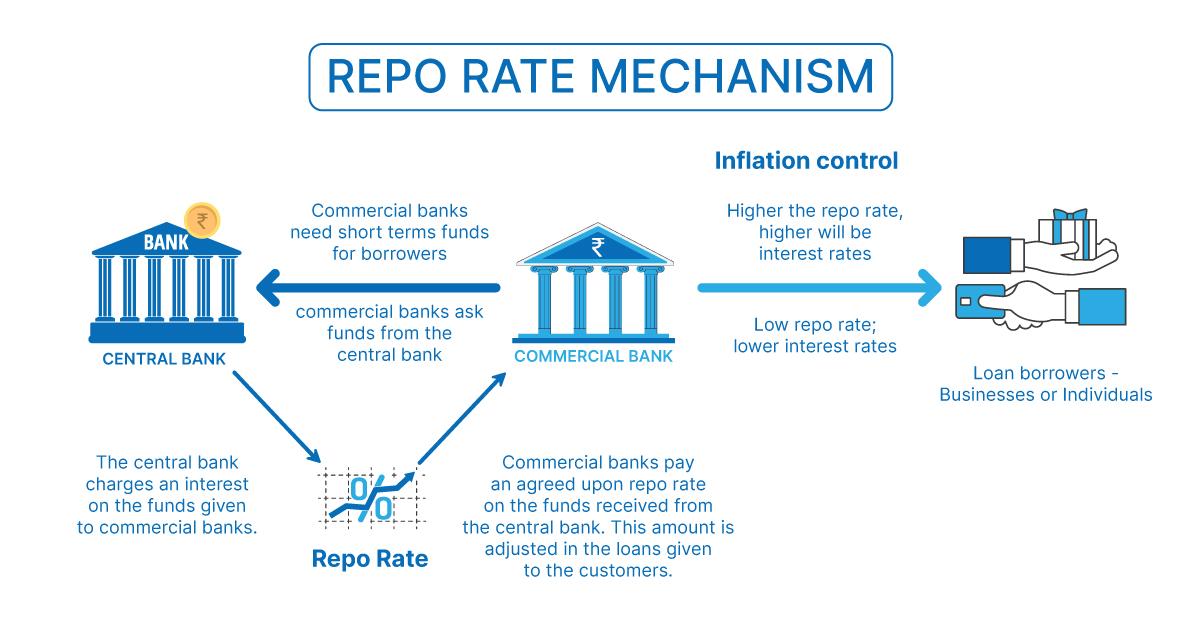

1. Opt for Repo-Rate-Linked Loans

- Repo-rate-linked loans are tied directly to the Reserve Bank of India's (RBI) repo rate.

- When the repo rate drops, your home loan interest rate decreases automatically.

- Always check if your lender offers this facility, as it ensures you benefit from any rate cuts in the economy.

Repo-Rate Definition

Repo-Rate Definition

2. Make Prepayments Whenever Possible

- Prepaying even a small portion of your home loan can reduce the outstanding principal, directly lowering interest costs.

- Target prepayments early in the tenure when the interest portion of your EMI is the highest.

- Most lenders do not charge prepayment penalties on floating-rate loans, so use this to your advantage.

3. Switch to a Shorter Tenure

- While shorter tenures result in higher EMIs, they drastically reduce the total interest you pay over time.

- For example, a 20-year loan tenure will accrue more interest than a 10-year tenure.

- If possible, consider adjusting your repayment plan to pay off your loan faster.

4. Increase Your EMI Amount Gradually

- As your income grows, use the opportunity to increase your EMI contributions.

- A higher EMI reduces your outstanding balance faster, directly impacting interest savings.

- Many lenders allow borrowers to revise EMI amounts annually.

5. Transfer Your Loan to a Lower-Rate Lender

- If your current lender offers higher interest rates, explore transferring your loan to a different lender with lower rates.

- This process, known as a balance transfer, can save you lakhs over the loan tenure.

- Before switching, consider the associated costs, such as processing fees, and ensure the savings outweigh the expenses.

6. Park Surplus Funds in Super Saver Home Loans

- Super saver home loans let you link a savings account to your home loan.

- The funds in this account offset the loan principal, reducing interest calculations.

- This is an excellent option if you frequently have surplus funds or variable income.

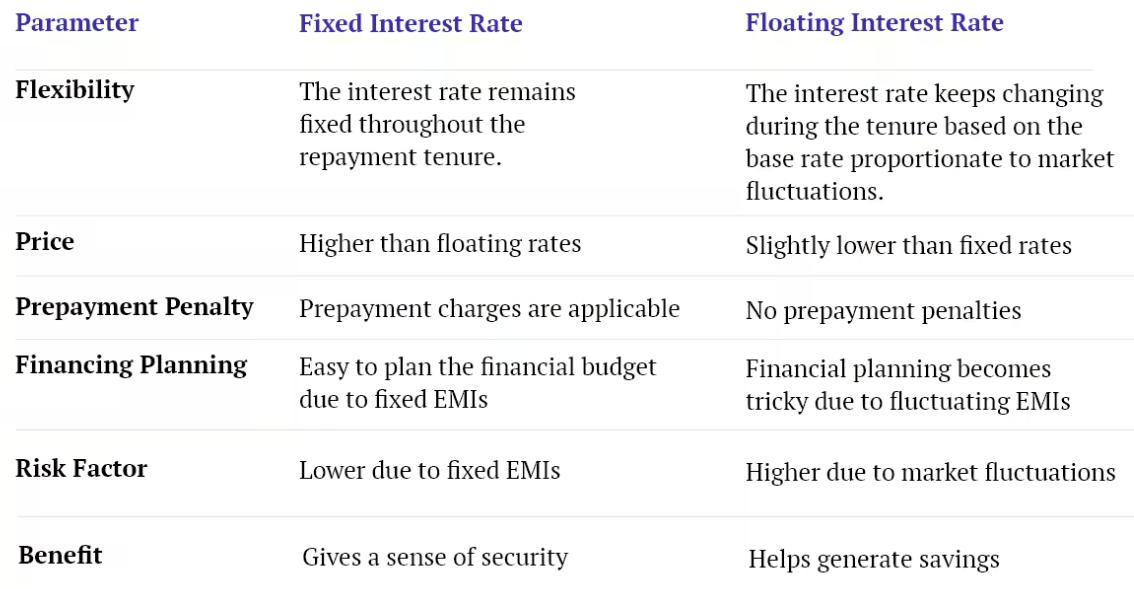

7. Choose Floating Over Fixed Rates

- Floating interest rates are usually lower than fixed rates and can decrease further when market rates fall.

- Fixed rates are stable but tend to be higher, making floating rates a better choice for long-term savings.

Floating Vs. Fixed Rates

Floating Vs. Fixed Rates

8. Negotiate with Your Lender

- Don't hesitate to ask your lender for a lower interest rate, especially if you've been a responsible borrower.

- Highlight a good credit score (750 or higher), timely payments, and other positive financial indicators to strengthen your case.

9. Monitor Market Trends

- Interest rates fluctuate based on economic conditions and RBI policies.

- Stay informed about repo rate changes and budget announcements that might impact rates.

10. Avoid Delayed Payments

- Late payments can attract penalties and higher interest rates.

- Set up auto-debit for your EMI to ensure timely payments and maintain a good credit score.

Credit Score Range

Credit Score Range

Conclusion

Reducing home loan interest is not just about choosing the right lender, it's about proactively managing your loan throughout its tenure. By prepaying strategically, switching to repo-rate-linked loans, or opting for shorter tenures, you can save a substantial amount of money. Every small step you take towards reducing your interest burden adds up in the long run, helping you achieve financial stability and enjoy your dream home without unnecessary stress.

explore further

Latest from Home Buying Tips

More from Recommendations

Resources

Dwello, for every home buyer, is a way to go from 'I feel' to 'I know', at no extra cost.